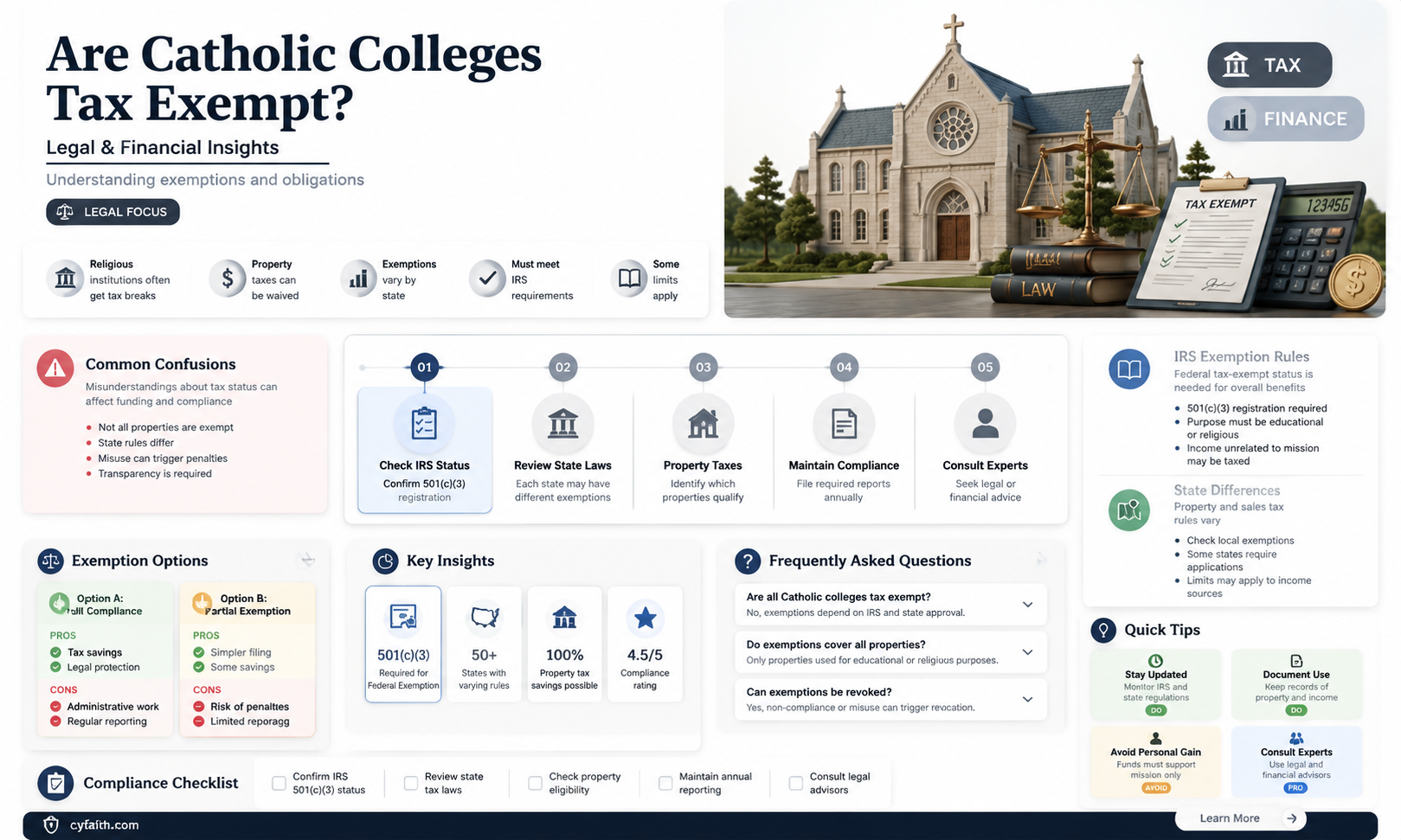

Catholic colleges, like many other religious and educational institutions, often enjoy tax-exempt status under U.S. law, primarily due to their classification as nonprofit organizations under Section 501(c)(3) of the Internal Revenue Code. This exemption is granted because these institutions are deemed to serve public purposes, such as education and religious activities, which align with broader societal benefits. However, the tax-exempt status of Catholic colleges has occasionally sparked debate, with critics questioning whether their religious affiliations or substantial endowments should disqualify them from such privileges. Proponents argue that these institutions provide significant educational and community contributions, justifying their exemption. Understanding the criteria and implications of this tax status is essential for assessing the role of Catholic colleges within the broader educational and fiscal landscape.

| Characteristics | Values |

|---|---|

| Tax Exemption Status | Catholic colleges in the U.S. are generally tax-exempt under Section 501(c)(3) of the Internal Revenue Code, as they are classified as religious and educational organizations. |

| Eligibility Criteria | To qualify, the college must be organized and operated exclusively for religious and educational purposes, and no part of its net earnings can benefit private individuals. |

| Property Tax Exemption | Most Catholic colleges are exempt from property taxes on buildings and land used for educational and religious purposes. |

| Sales and Use Tax Exemption | Exempt from sales and use taxes on purchases related to their exempt purposes, such as educational materials and supplies. |

| Income Tax Exemption | Exempt from federal income tax on income generated from activities related to their exempt purposes, including tuition, donations, and investments. |

| Unrelated Business Income Tax (UBIT) | Subject to UBIT on income from activities not substantially related to their exempt purposes, but many educational activities are excluded. |

| State-Specific Variations | Tax exemptions can vary by state, with some states imposing additional requirements or limitations on exemptions for religious and educational institutions. |

| Public Benefit Requirement | Must demonstrate that they serve a public benefit, such as providing education, to maintain their tax-exempt status. |

| Reporting Requirements | Required to file annual information returns (Form 990) with the IRS to maintain transparency and compliance. |

| Potential Revocation | Tax-exempt status can be revoked if the organization fails to meet the requirements or engages in prohibited activities, such as political campaigning. |

Explore related products

What You'll Learn

![]()

Legal Basis for Exemption

Catholic colleges in the United States are generally tax-exempt under Section 501(c)(3) of the Internal Revenue Code (IRC), which grants tax-exempt status to organizations operated exclusively for religious, charitable, scientific, or educational purposes. This exemption is rooted in the First Amendment's protection of religious freedom and the establishment clause, which prohibits the government from favoring or disfavoring any particular religion. To qualify for this status, Catholic colleges must meet specific criteria, including being organized and operated exclusively for exempt purposes, not engaging in substantial lobbying activities, and not participating in political campaigns.

The legal basis for tax exemption is further supported by the U.S. Supreme Court’s interpretation of the First Amendment. In cases such as *Walz v. Tax Commission of the City of New York* (1970), the Court upheld property tax exemptions for religious organizations, including religious schools, as a means of avoiding excessive entanglement between government and religion. The Court reasoned that such exemptions do not constitute an establishment of religion but rather ensure that religious institutions are not unfairly burdened by taxation, which could impede their ability to function.

Additionally, the IRC provides specific provisions for educational institutions, including Catholic colleges, under Section 501(c)(3). These institutions must demonstrate that their primary purpose is educational and that they serve a public benefit. Catholic colleges often meet these requirements by providing higher education to students, conducting research, and contributing to the broader community through service and outreach programs. The IRS evaluates these institutions based on factors such as curriculum, faculty qualifications, and adherence to educational standards.

State laws also play a role in the tax-exempt status of Catholic colleges. Many states automatically grant tax exemptions to organizations that are exempt under federal law, while others require separate applications or compliance with additional state-specific criteria. For example, property tax exemptions for educational institutions are often governed by state statutes, which may require proof of nonprofit status, educational mission, and financial accountability. Catholic colleges must navigate both federal and state regulations to maintain their tax-exempt status.

Finally, the legal framework for tax exemption includes oversight and compliance mechanisms. The IRS monitors tax-exempt organizations, including Catholic colleges, to ensure they continue to meet the requirements for exemption. This includes filing annual information returns (Form 990) and maintaining records that demonstrate adherence to exempt purposes. Failure to comply with these requirements can result in the loss of tax-exempt status, penalties, or other legal consequences. Thus, Catholic colleges must remain vigilant in their operations to ensure ongoing compliance with federal and state tax laws.

Robert Jeffress' Controversial Remarks: Catholics and Salvation Explained

You may want to see also

Explore related products

$15.22 $24.99

![]()

IRS Requirements for Nonprofits

Catholic colleges, like many other educational institutions, often seek tax-exempt status under the U.S. Internal Revenue Code (IRC) Section 501(c)(3). To qualify for this status, these institutions must meet specific IRS requirements for nonprofits. The IRS mandates that organizations operate exclusively for charitable, educational, religious, or scientific purposes, and Catholic colleges typically fall under the educational and religious categories. However, merely being affiliated with the Catholic Church or offering religious education is not sufficient; the institution must demonstrate that its primary purpose aligns with IRS criteria for tax exemption.

One of the key IRS requirements for nonprofits is the prohibition of inurement, which means that no part of the organization's net earnings can benefit private individuals, shareholders, or other insiders. Catholic colleges must ensure that their operations do not result in private benefit, even if they are affiliated with a religious entity. Additionally, these institutions must avoid engaging in political campaign activities or substantial lobbying, as such actions can jeopardize their tax-exempt status. Compliance with these rules is essential to maintain eligibility for tax exemption.

Another critical aspect of IRS requirements for nonprofits is the necessity for Catholic colleges to be organized and operated exclusively for exempt purposes. This includes adopting bylaws or other governing documents that explicitly state the organization's exempt purpose and ensuring that all activities further that purpose. For example, a Catholic college must demonstrate that its curriculum, admissions policies, and operational practices are consistent with its educational mission. Any activities that do not align with this mission could raise concerns with the IRS.

Financial accountability is also a cornerstone of IRS requirements for nonprofits. Catholic colleges must maintain detailed financial records and file annual information returns, such as Form 990, to disclose their financial activities, governance practices, and compliance with tax laws. Transparency in financial reporting not only satisfies IRS mandates but also builds trust with donors, students, and the public. Failure to file required forms or provide accurate information can result in penalties or loss of tax-exempt status.

Lastly, the IRS requires nonprofits, including Catholic colleges, to adhere to public charity status rules, which often involve meeting specific public support tests. These tests ensure that the organization receives a substantial portion of its funding from diverse public sources rather than a single individual or entity. Catholic colleges can meet these requirements through tuition payments, donations from a broad base of supporters, and grants from government or private foundations. By fulfilling these IRS requirements, Catholic colleges can maintain their tax-exempt status while advancing their educational and religious missions.

Embracing God's Love: A Catholic Guide to Self-Love and Acceptance

You may want to see also

Explore related products

$36.75 $39.95

![]()

Role of Religious Affiliation

The role of religious affiliation is pivotal in understanding why Catholic colleges are often tax-exempt. In the United States, religious institutions, including colleges and universities, are generally granted tax-exempt status under Section 501(c)(3) of the Internal Revenue Code. This exemption is rooted in the First Amendment's protection of religious freedom and the separation of church and state. Catholic colleges, as extensions of the Catholic Church, are considered religious organizations, which inherently qualifies them for this tax status. Their affiliation with the Church is not merely symbolic; it is a foundational aspect of their identity, mission, and operations, aligning them with the broader category of religious entities that are shielded from federal income tax.

The religious affiliation of Catholic colleges is further evidenced by their adherence to Catholic doctrine and values, which permeate their academic programs, campus life, and governance structures. These institutions often incorporate religious education, require participation in spiritual activities, and maintain ties to diocesan or religious orders. Such practices reinforce their religious character, a key criterion for tax exemption. The IRS evaluates whether an organization’s activities are primarily religious in nature, and Catholic colleges typically meet this standard by integrating faith into their core functions. This integration is not incidental but central to their purpose, distinguishing them from secular institutions and justifying their tax-exempt status.

Another critical aspect of religious affiliation is the governance and control exerted by the Catholic Church over these colleges. Many Catholic institutions are overseen by bishops, religious orders, or other Church authorities, ensuring that their operations remain consistent with Catholic teachings. This ecclesiastical governance is a significant factor in maintaining their religious identity and, by extension, their eligibility for tax exemption. The IRS recognizes that such control by a religious body is a strong indicator of an organization’s religious nature, further solidifying the case for tax-exempt status. Without this affiliation and oversight, Catholic colleges might be viewed as secular educational entities, subject to different tax regulations.

Moreover, the religious affiliation of Catholic colleges often extends to their funding and support systems. Many rely on donations from Catholic dioceses, parishes, and individual Catholics, as well as grants from Church-affiliated foundations. This financial dependence on religious sources underscores their status as part of the broader Catholic community. The IRS considers such funding patterns when determining tax exemption, as they demonstrate the institution’s integration into a religious framework. In contrast, institutions without this religious backing would likely lack the same basis for exemption.

Finally, the role of religious affiliation in Catholic colleges’ tax-exempt status is reinforced by legal precedents and court rulings. Courts have consistently upheld the tax-exempt status of religious educational institutions, emphasizing the importance of their religious character and mission. For Catholic colleges, this means that their affiliation with the Church is not just a historical or cultural relic but a legally recognized attribute that qualifies them for exemption. Challenges to this status are rare and typically unsuccessful, as the religious nature of these institutions is well-established and protected under law. Thus, religious affiliation is not merely a label but a substantive and determinative factor in the tax treatment of Catholic colleges.

Understanding the Catholic Easter Duty: Obligations and Significance Explained

You may want to see also

Explore related products

$13.94 $14.99

![]()

State vs. Federal Tax Laws

Catholic colleges, like many religious and educational institutions, often benefit from tax-exempt status, but the specifics of this exemption depend on the interplay between state and federal tax laws. At the federal level, the Internal Revenue Code (IRC) Section 501(c)(3) grants tax-exempt status to organizations operated exclusively for religious, charitable, scientific, or educational purposes. Catholic colleges typically qualify under this provision because they are nonprofit entities aligned with the Catholic Church’s mission and provide educational services. To maintain this status, they must meet strict criteria, such as not engaging in political campaigning or distributing profits to private individuals. Federally, this exemption applies to income tax, but it does not automatically exempt the institution from other federal taxes, such as payroll taxes for employees.

In contrast, state tax laws vary significantly and can either align with or diverge from federal regulations. Many states conform to federal tax-exempt status, meaning if a Catholic college is exempt under Section 501(c)(3), it is also exempt from state corporate income tax. However, states have their own criteria for granting additional exemptions, such as property taxes. For example, some states exempt religious and educational institutions from property taxes on buildings and land used for educational purposes, while others may require the institution to apply for an exemption and meet specific state-defined standards. This variance means that a Catholic college might be fully tax-exempt in one state but subject to certain taxes in another, depending on local laws.

Another key difference lies in sales and use taxes. While federal law does not impose a general sales tax, states and localities do. Catholic colleges may be exempt from paying sales tax on purchases related to their educational mission in some states, but this is not guaranteed. For instance, a state might exempt textbooks or classroom equipment but require the college to pay sales tax on administrative supplies or non-educational items. Similarly, exemptions from use taxes—which apply to out-of-state purchases—depend entirely on state regulations, creating a complex landscape for institutions operating across multiple states.

State and federal laws also differ in their treatment of unrelated business income tax (UBIT). Federally, if a Catholic college generates income from activities not related to its educational purpose (e.g., renting out facilities for non-educational events), it must pay UBIT on that income. States may or may not impose a similar tax, and the definition of "unrelated business activity" can vary. This discrepancy requires colleges to carefully navigate both federal and state requirements to ensure compliance and avoid unexpected tax liabilities.

Finally, state incentives and credits can further complicate the tax landscape for Catholic colleges. Some states offer additional tax benefits, such as credits for scholarships provided to low-income students or exemptions for specific programs, while others may impose unique taxes or fees on nonprofit institutions. These state-specific provisions underscore the importance of understanding local laws in addition to federal regulations. In summary, while federal law provides a foundational framework for tax exemption, the true tax obligations of Catholic colleges are shaped by the unique interplay of state and federal tax laws, requiring careful consideration and often professional guidance.

The Ancient Roots of the Word 'Catholic

You may want to see also

Explore related products

![]()

Impact on Tuition Costs

Catholic colleges' tax-exempt status significantly influences tuition costs, primarily by reducing operational expenses that might otherwise be passed on to students. As nonprofit institutions, these colleges are exempt from federal and state income taxes, property taxes, and in some cases, sales taxes. This exemption allows them to allocate more resources to academic programs, scholarships, and campus maintenance rather than tax payments. For students, this translates to potentially lower tuition fees compared to for-profit institutions, as the colleges are not burdened by additional tax liabilities that could inflate operational costs.

The tax-exempt status also enables Catholic colleges to invest in financial aid programs, which directly impacts tuition affordability. By saving on taxes, these institutions can offer more scholarships, grants, and work-study opportunities to students from diverse socioeconomic backgrounds. This financial aid reduces the net cost of attendance for many students, making higher education more accessible. Without tax exemptions, colleges might have fewer resources to fund such programs, leading to higher out-of-pocket expenses for students and their families.

However, the impact on tuition costs is not uniform across all Catholic colleges. Some institutions, particularly those with large endowments or significant donor support, may still charge higher tuition rates despite their tax-exempt status. This is often due to the cost of maintaining high-quality facilities, faculty, and specialized programs. Nonetheless, even in these cases, the tax exemption helps prevent tuition from rising even further, as the colleges are not compelled to offset additional tax burdens through increased fees.

Another factor to consider is how tax exemptions influence the overall financial health of Catholic colleges. By reducing expenses, these institutions can maintain stability during economic downturns or periods of declining enrollment. This stability is crucial in avoiding sudden tuition hikes, which can occur when colleges face financial strain. Thus, the tax-exempt status indirectly supports predictable and manageable tuition costs over time, benefiting both current and prospective students.

In summary, the tax-exempt status of Catholic colleges plays a pivotal role in shaping tuition costs by lowering operational expenses, enabling robust financial aid programs, and fostering long-term financial stability. While it does not guarantee uniformly low tuition rates, it helps mitigate cost increases and ensures that more students can afford a Catholic education. Understanding this relationship is essential for students and families evaluating the affordability of these institutions.

Salvation Steps for Catholics: What You Need to Know

You may want to see also

Frequently asked questions

Not all Catholic colleges are automatically tax exempt. To qualify, they must meet specific criteria set by the IRS, such as being organized and operated exclusively for educational purposes and not engaging in activities that benefit private interests.

A Catholic college must be recognized as a 501(c)(3) organization by the IRS, which requires it to be nonprofit, operate primarily for educational purposes, and not engage in political campaigning or excessive lobbying.

Generally, Catholic colleges are exempt from paying property taxes on buildings and land used for educational purposes, as long as they maintain their tax-exempt status under 501(c)(3). However, they may still pay taxes on properties not directly related to their educational mission.